|

|

|

|

|

|

"Courage looks like stupidity to an audience of maximizers"

|

|

|

|

|

|

|

If you enjoy or get value from The Interesting Times, I'd really appreciate it if you would support it by forwarding it to a friend or sharing it wherever you typically share this sort of thing - (Twitter, LinkedIn, Slack groups, etc.)

|

|

|

|

|

Happy Halloween!

I have a 1.5-year-old, so I will be doing something vaguely resembling trick-or-treating for the first time in a while this year.

I’m considering switching email software for this newsletter and some other writing I’ve been working on. It would be helpful to know where my readers (that's you!) currently read on the internet to figure out how to make it most accessible. Do you read in your email? The browser? A Read it later app? A dedicated app like Substack? If you have a minute, hit reply and let me know.

My friends at Monetary Metals are hiring a Marketing Communications and Operations Manager. The role is heavily focused on email marketing, take a look if that’s up your alley.

|

|

|

American Affairs

Like everyone else, I’ve been thinking about AI and its impacts. This article looks at it through a Schumpeterian lens of how past technological and economic periods have shifted.

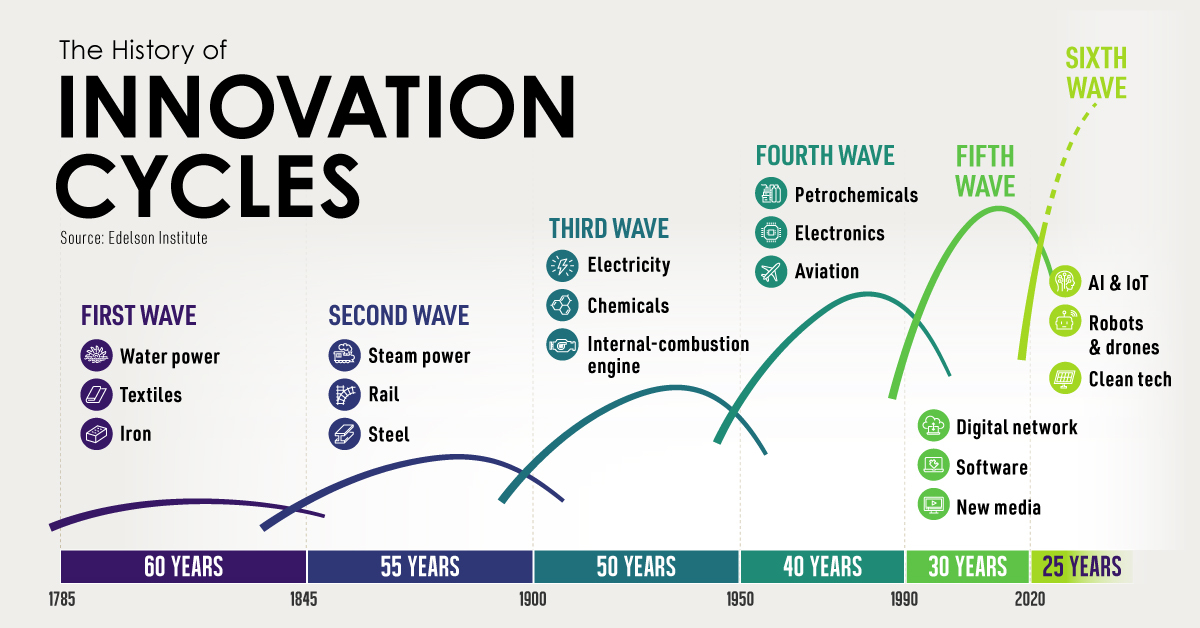

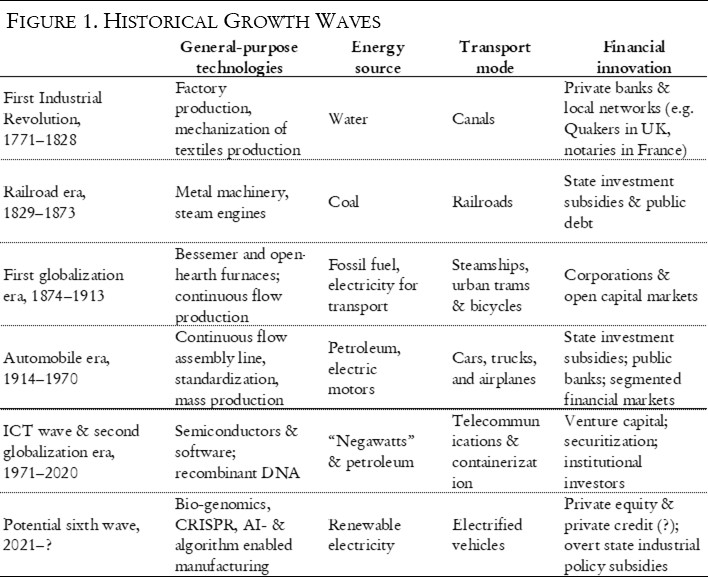

Joseph Schumpeter saw capitalism as characterized by periods of "creative destruction"—waves of innovation that simultaneously generate rapid growth and render entire industries obsolete.

This seems obviously true, and a lot of standard economic thinking more or less treats innovation as a side dish rather than the main course.

Schumpeter identified different historical periods of explosive growth driven by new technologies. Each wave followed a predictable arc—emergence, rapid expansion, maturity, and eventual exhaustion as the core technologies reached saturation and competitive advantages eroded.

|

|

|

|

|

*Note: Random image from the internet to give you an idea of the concept, neither he nor I necessarily agree with these particular categorizations.

|

|

|

More recently, Carlota Perez expanded this framework by adding social dimensions that Schumpeter underemphasized. Her "techno-economic paradigm" incorporates five M's: making (production methods), moving (transportation), marketing (distribution), macro-managing (governance and regulation), and mindset (cultural common sense about best practices). This captures an important component Schumpeter undervalued: technological revolutions require complementary institutional and social transformations to achieve their full economic potential.

|

|

|

|

|

Perez's model explains why tech adoption follows an S-curve pattern. New technologies emerge during crisis periods when existing paradigms exhaust themselves, go through lengthy "installation periods" where early adopters experiment with applications, then enter "deployment periods" of widespread adoption and productivity gains. The gap between technological possibility and economic transformation often spans decades because societies must rebuild their institutional architecture around new ways of doing business.

The automobile era required the internal combustion engine, but it also required building a global supply chain around oil, nation-states building road systems, and (to some extent) people moving to the suburbs. Social and technological change have to happen together. Owning a car without being able to get gas or drive on a road is not very useful.

This article looks at the current moment and argues we are at a turning point, the exhaust of the fifth wave (launched by Intel's 1971 microprocessor and the Cohen-Boyer recombinant DNA breakthrough) and the emergence of the sixth wave: AI for labor automation and materials design, renewable energy for electrification, CRISPR and mRNA for precision medicine, and synthetic biology for sustainable manufacturing.

The fifth wave has become characterized by the tripartite franchise model, which involves three players:

- Lead firms owning all the IP

- Supplier/Manufacturer networks that are capital-intensive

- Producers that are labor-intensive

Lead firms like Apple or Nike own massive intellectual property portfolios and maintain small, highly compensated workforces focused on design, marketing, and IP development.

These firms then orchestrate complex supplier networks consisting of capital-intensive second-layer manufacturers (think Foxconn or TSMC) and labor-intensive third-layer producers are scattered across emerging markets.

Lead firms exercise de facto control over entire value chains while owning minimal physical assets and maximizing profits while minimizing operational risk.

The global geography of this system reveals its underlying logic. Lead firms concentrated mostly in specific U.S. regions (Silicon Valley, Seattle, NYC, etc.) where they could access top talent and capital. Capital-intensive manufacturing migrated to Japan, Europe, and parts of China with advanced industrial capabilities.

Labor-intensive production scattered across emerging markets with favorable wage structures. This wasn't random—it represented the optimal allocation of different production stages within a legal and financial framework designed to maximize returns to IP ownership.

Some signs of exhaustion of this paradigm:

- Smartphone unit sales peaked in 2018—the exemplary consumer product of the fifth wave has saturated its addressable market. Growth now comes from price increases rather than volume expansion, tethered to population growth rather than market creation.

- Digital advertising, which funded the platform giants, has similarly matured outside of streaming video.

- The tech giants announced $191 billion in share buybacks from June 2023 to June 2024 rather than investing in new productive capacity. When lead firms return cash to shareholders instead of expanding output, the growth wave is over.

This is to be expected. Each paradigm experiences endogenous decay—the relationships that initially drove growth eventually constrain it. The Fordist assembly line era died when it exhausted cheap oil and docile workers; OPEC's formation coincided with labor organizing that challenged the monotonous pace of production lines.

Today's franchise model faces similar internal contradictions. The high-skilled workers who power tripartite structures are pricing themselves out of sustainability, while the IP-intensive nature of leading industries creates winner-take-all dynamics that undermine broad-based growth.

I found the "tripartite structure" idea to encapsulate a lot about the modern world and you can also see how the post-Covid, tariff world doesn't really jive with this structure. So what's next?

The sixth wave technologies are already visible:

- AI for labor automation and materials design

- Renewable energy for electrification

- CRISPR and mRNA for precision medicine

- Synthetic biology for sustainable manufacturing

But, as Perez pointed out, technology alone doesn't create growth waves—social and institutional transformation determines success. You need everything to work together. So how does it all play out?

One possibility is AI's massive power consumption matches with renewable cost curves following Wright's Law. Supercomputers can be co-located with solar and wind installations, providing consistent demand for intermittent generation while avoiding grid transmission costs. This solves two problems simultaneously: AI needs cheap, reliable power, and renewables need predictable load to justify investment. Maybe throw in some nuclear energy there as well, assuming the regulatory winds keep shifting that way.

I suspect crypto plays a bigger role in this transition than this analysis suggests. Blockchain infrastructure could provide coordination mechanisms while enabling new financing models through tokenization. The organizational possibilities of programmable money and automated contracts on a credibly neutral platform may be as transformative as the underlying computational technologies.

One big question here is how much AI will drive growth.

The AI optimists often suggest GDP growth will accelerate to 10% or 20% from its long-run historical average of around 3%. It’s hard to overstate how big of a deal that would be.

My personal intuition is that a lot of these people probably under-appreciate the institutional component of growth. Self-driving cars and AI radiology is probably more than adequate technologically already or will be very soon but adoption will move at the speed of government and regulatory reform (read: slow).

The article presents three scenarios, but the most plausible involves extended turbulence as old and new paradigms battle for dominance. Bottlenecks in commodity supply chains, energy security challenges, U.S.-China technological competition, and domestic political dysfunction could create persistent instability even as breakthrough technologies mature. The barrier isn't so much technological maturity but institutional incapacity—our ability to build organizations and governance structures that get the best and most out of emerging technologies. Broadly, our world seems to be lacking innovation in social technology more than physical technology.

Ep.444: China’s Quest to Engineer the Future | Dan Wang [Podcast]

Hidden Forces

Dan Wang argues China’s approach is best understood as an "engineering state" optimized for building infrastructure and diffusing technology, while America has evolved into a "lawyerly society" that excels at protecting what exists while obstructing new development.

I find this much more explanatory than the rather stale "communist vs. capitalist" or "left vs. right" frameworks.

If you look at the CCP leaders, it’s mostly engineers and mega-project managers. If you look at the U.S. Executive and Legislative branches, it’s mostly lawyers. This leads to a completely different approach to how problems are conceptualized and solved.

Wang suggests regulatory turn in 1960s America deserves more attention than it typically gets. Ralph Nader and elite law students reframed government as the problem rather than the solution—ironically adopting the same posture Reagan would later champion. This consumer protection movement, however necessary it seemed at the time, inaugurated our current era of litigation over construction.

The Second Avenue Subway was proposed in the 1920s, construction began in 1972 but was halted in 1975 due to fiscal crisis. Work restarted in 2007, and Phase 1 finally opened on January 1, 2017 —roughly 95 years after the initial proposal. That first phase delivered just three stations across 1.8 miles for $4.45 billion, approximately $2.5 billion per mile.

By contrast, The Shanghai Metro started in 1993 and has grown to become the world's second-longest metro system at 502 miles with 508 stations. There are many such examples.

I do wonder if there is a robustness/efficiency tradeoff between the American and Chinese systems. Sometimes short term efficiency comes at the cost of long-term robustness. My reading of the American system (and liberal democracy more broadly) is essentially that it was willing to trade off a lot of efficiency to get more robustness. The distinction is not as one dimensional as that, but I think there is a lot there.

It also seems like the Chinese are hyper aware of the fragility of their system. They study disasters like Chernobyl not as engineering failures but as political ones—moments when natural catastrophes trigger regime collapse. This creates an "apocalyptic element" where survival demands constant vigilance. Andy Grove's "only the paranoid survive" is the operating system of the Chinese Communist Party.

I also liked the observation of commonalities between Americans and Chinese: both share a hustle mentality and appreciation for what he calls the "technological sublime"—the Golden Gate Bridge, the Apollo missions, massive engineering achievements that inspire awe. Europeans and Japanese pursue perfection and comfort; Americans and Chinese pursue scale and disruption.

East Asia broadly when I spent a lot time there in the 2010s felt like the frontier in a way I somewhat imagine the American West did in the late 1800s and into the early 1900s.

The TL:DR; A Chinese-dominated world order means censorship, social engineering, and distrust of independent institutions—values incompatible with pluralism. The better path for America isn't deterring China through containment but answering its own people's needs: building housing in expensive cities, expanding energy capacity, and restoring physical order

Statecraft

Perhaps apartment buildings are a microcosm of the U.S.’s inability to build the infrastructure it needs? Post 2008, Fannie Mae and Freddie Mac lending policies pushed developers toward studio and one-bedroom units optimized for roommate-sharing rather than child-rearing.

Private equity funds deploying capital on 2-3 year horizons don't care what happens to neighborhood composition in a decade. They care about lease-up velocity and exit multiples. Studios turn over twice as fast as three-bedrooms, generating higher yields for the fund timeline. Charlie Munger's dictum applies: show me the incentive, I'll show you the outcome.

What families actually want is straightforward—they'd trade bathroom count, kitchen size, and open floor plans for a third bedroom where their kid can sleep. Pre-war apartments understood this. A 1,200 square foot three-bedroom with one bathroom served families better than a modern 1,200 square foot two-bedroom with 2.5 baths and a kitchen sized for hosting Thanksgiving dinner parties that never happen.

The policy implications cut against easy YIMBY orthodoxy. Upzoning alone won't fix this—it'll just generate more studios because the rental arithmetic still favors them. A 400 square foot studio at $1,200/month ($3 per square foot) works anywhere. But $3 per square foot on a 1,500 square foot family apartment means $4,500 rent, which prices out most households.

Housing is perhaps constrained more by its financing structure than its physical inputs. Until we align investor time horizons with the 10-20 year timescales on which neighborhood composition matters, cities will continue hemorrhaging families—not because they're inherently incompatible with children, but because our capital markets are optimized for the wrong outputs.

David Foster Wallace unedited interview (2003) [Interview]

Manufacturing Intellect

I have read much of David Foster Wallace’s literary work and listened to many of his interviews and found myself coming back to this 2003 interview on American culture.

There is so much to unpack that I will, out of a combination of incompetence and laziness, not attempt to do so beyond to say that I find his view on American culture resonated two decades later.

To be sentimental, The nostalgia I have for so thoughtful an observer is particularly strong in our current cultural moment.

Solving the Equity Premium Puzzle, and Uncovering a Huge Flaw in Investment Theory [Article]

Breaking The Market

One of the biggest puzzles in classical financial theories is the equity premium puzzle—why do stocks return 6% more than treasury bills? If people were ‘rational,’ wouldn’t they just own more stocks?

The most well accepted explanations for this tend to be behavioral. A common explanation is that loss aversion leads to people selling at the worst times or not being willing to hold too much because they know stocks can go down 50%+ in a crisis.

However, this piece argues that something more fundamental is happening. The comparisons are simply not comparing like for like. Most studies of the equity premium measure individual treasury bills against the S&P 500 index (or a similar index), treating a single asset and a portfolio of assets as equivalent.

However, the S&P 500 is not the same thing as stocks. Because of the diversification and rebalancing factors, it is significantly better performing on a risk-adjusted basis than a typical single stock.

Individual stocks carry 30-35% standard deviation, roughly 50% more volatile than the S&P 500's 20%. When you account for this higher volatility and convert from arithmetic to geometric returns—the only returns investors actually experience through compounding—the equity premium of individual stocks drops to about 0.55%, essentially converging with the risk-free rate.

The author uses a useful metaphor: It’s like asking why a single 400-meter runner is slower than a 4x100 relay team. One combines multiple participants who tag in and out (like an index rebalancing), the other is a solo performance. They're categorically different.

The S&P 500's return tells you nothing about what happens to individual stocks—a point reinforced by research showing 58% of common stocks don't even keep pace with treasury bills over time.

I think the behavioral factors probably play in, but this explanation seems probably pretty important and not well appreciated. To what extent are many risk premia really just rebalancing premiums in disguise? Is it rebalancing’s free lunch all the way down?

|

|

|

|

|

As always, if you're enjoying The Interesting Times, I'd love it if you shared it with a friend (or three). You can send them here to sign up. I try to make it one of the best emails you get every week and I'm always open to feedback on how to better do that.

If you'd like to see everything I'm reading, you can follow me on Twitter or LinkedIn for articles and podcasts. I'm on Goodreads for books. Finally, if you read anything interesting this week, please hit reply and send it over!

|

|

|

|

|

The Interesting Times is a short note to help you better invest your time and money in an uncertain world as well as a digest of the most interesting things I find on the internet, centered around antifragility, complex systems, investing, technology, and decision making. Past editions are available here.

|

|

|

|

|

Here are a few more things you might find interesting:

Interesting Essays: Read my best, free essays on topics like bitcoin, investing, decision making and marketing.

Consulting & Advising: Are you looking for help with making decisions around scaling your company from $500k to $5 million? I’ve been working with authors, entrepreneurs, and startups for half a decade to help them get more out of their businesses.

Internet Business Toolkit: An exhaustive list of all the online tools I use to be more productive.

|

|

|

|

|